Freight Factoring: The Complete Guide for Brokers (2026)

Learn how freight factoring works for brokers, typical rates and advance terms, recourse vs non-recourse, compliance notes, and how to choose a factor.

Omar Draz

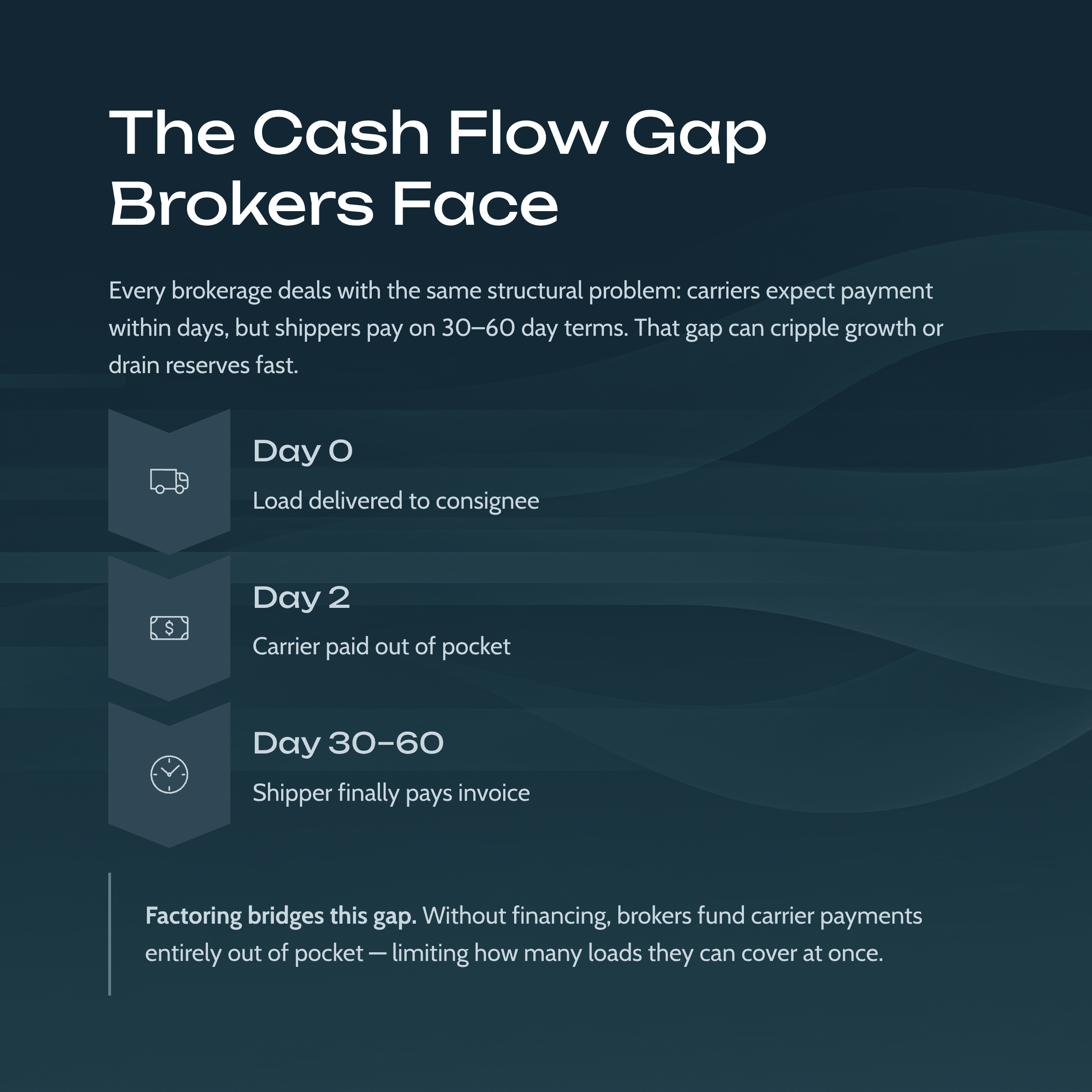

Freight brokerages live and die on timing. You might have to pay carriers fast (sometimes same day) while shippers take 30–60+ days to pay you. Freight factoring exists to cover that gap by turning your outstanding invoices into cash now.

This guide explains how freight factoring works for freight brokers, what it typically costs, the contract terms that matter, and what’s changed in the 2026 compliance landscape.

Not financial, legal, or tax advice. Use this as a practical starting point, then have your attorney/CPA review anything you sign.

What is freight factoring for brokers?

Freight factoring (for brokers) is a form of invoice factoring where your brokerage sells its unpaid shipper invoices (accounts receivable) to a factoring company in exchange for an upfront advance, then receives the remainder (minus fees) when the shipper pays.

Most factoring arrangements are built around three basics:

Advance rate: the percentage you get upfront

Reserve: the portion held back until the invoice is collected

Factoring fee (discount rate): what you pay for the service (often tied to how long the invoice takes to pay)

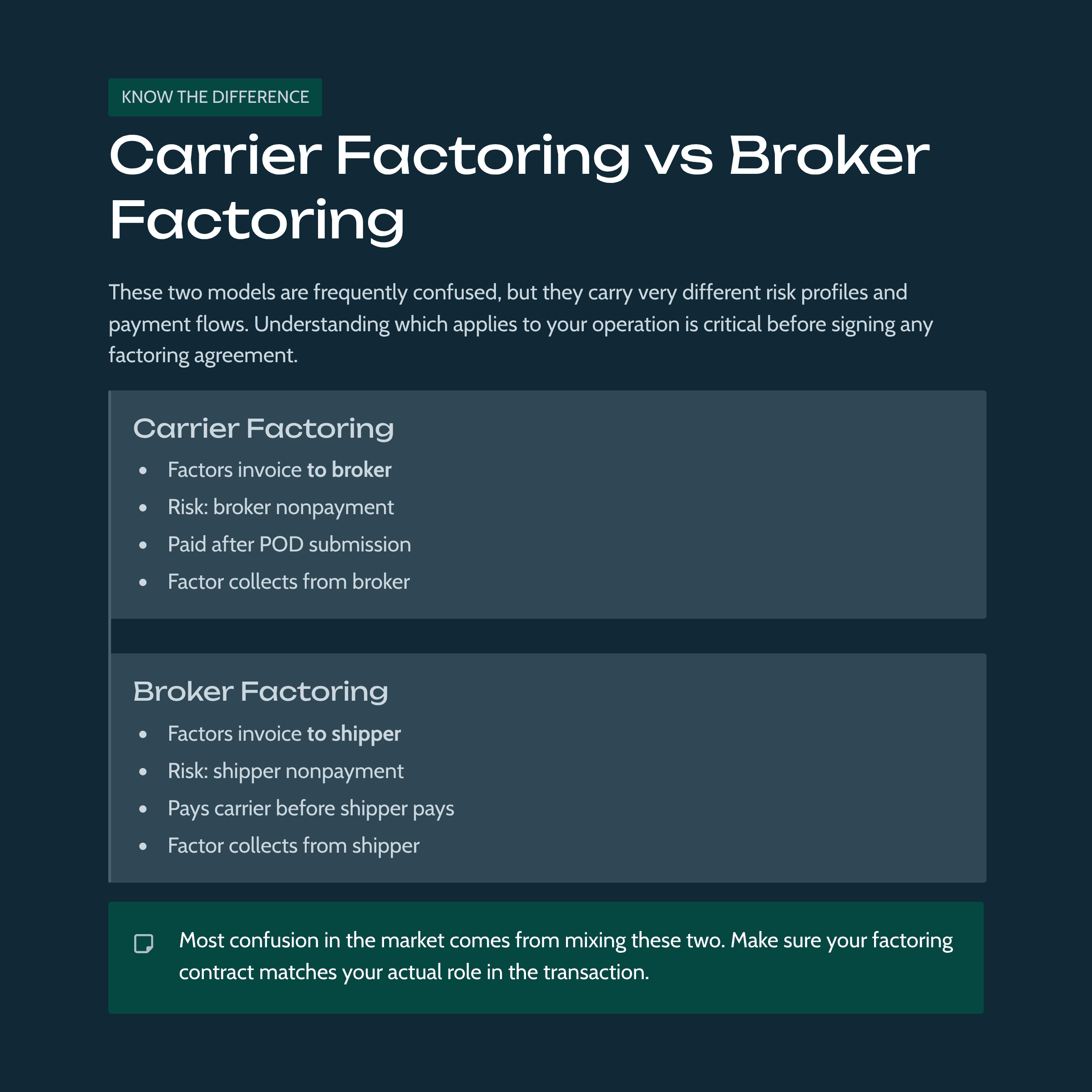

Freight factoring for brokers vs freight factoring for carriers (important)

A lot of articles use “freight factoring” to mean carrier factoring (truckers factoring invoices they bill to brokers). Broker factoring is different.

Carrier factoring (common)

Carrier hauls the load

Carrier factors the invoice they send to the broker

Factor collects from the broker

Broker factoring (what this guide is about)

Broker arranges the load, pays the carrier, bills the shipper

Broker factors the shipper invoice (your A/R)

Factor collects from the shipper

If you’re writing SOPs, training new ops staff, or comparing funding options, don’t mix these up. The paperwork, risk, and relationship dynamics are different.

Why brokers use freight factoring

Freight factoring is not just “emergency cash.” Brokers use it when they want predictable cash flow while scaling.

Common broker use cases:

Pay carriers faster even when shippers pay net-30/net-45/net-60.

Offer quick pay programs without draining your bank account.

Grow volume without waiting for retained earnings to catch up.

Stabilize cash flow during seasonal swings or when a big customer stretches terms.

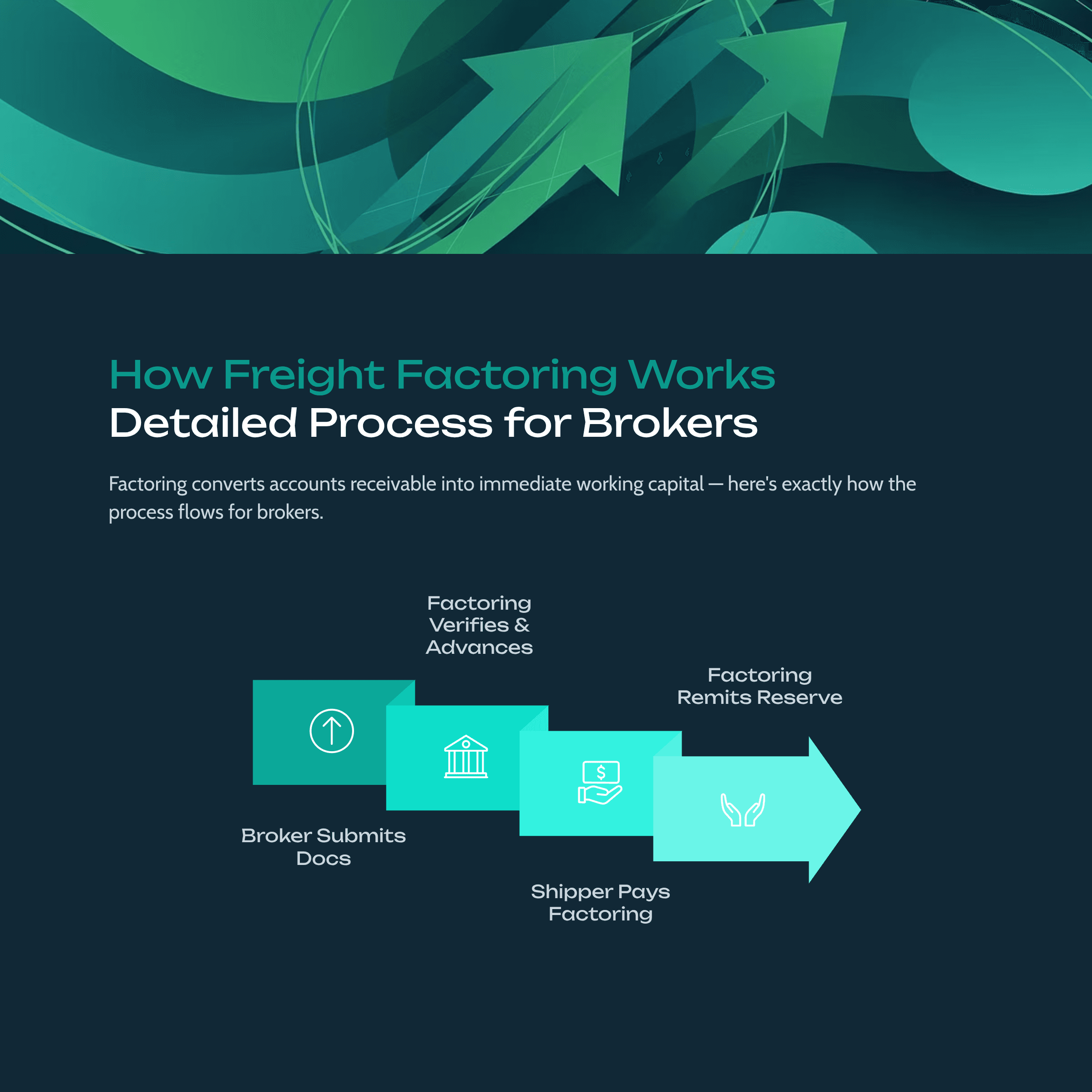

How freight factoring works for brokers (step-by-step)

Exact workflows vary, but the core process looks like this:

You deliver the service (load is completed) and you have your supporting docs (rate confirmation, POD, etc.).

You invoice the shipper as usual.

You submit the invoice + documents to the factoring company.

The factor verifies the paperwork and the shipper’s credit/approval.

You receive an advance (often the same day or within 24–48 hours, depending on program and cutoff times).

The factor collects payment from the shipper.

You receive the remainder (reserve) minus the factoring fee once payment clears.

One big operational change: in many setups, your shipper pays the factoring company directly (because the receivable has been assigned). That is normal, but you should decide upfront how you want that communication handled.

The freight factoring terms that actually matter

If you only read one part of this guide before you shop options, read this.

Advance rate (and what “100% advance” really means)

Advance rates commonly fall somewhere in the 70%–95% range, depending on the program, invoice type, and credit profile of the customer.

Some offers advertise “100%,” but that can simply mean fees are deducted differently (for example, taken out immediately instead of from a reserve). Don’t compare headline percentages without understanding fee timing.

Factoring fee (discount rate)

A simple rule of thumb: many factoring companies charge around 1% to 5% of the invoice value per month (or per 30 days), plus possible additional fees.

Industry-specific pricing varies. One 2025 breakdown listed transportation factoring rates in the ballpark of ~1.95%–4.0% (with advance rates often very high in some programs). Treat ranges as ranges, not promises.

Reserve

The reserve is the amount held until the shipper pays. If your program advances 90%, your reserve is typically the remaining 10%, minus adjustments (claims, short pays, accessorial disputes, etc.).

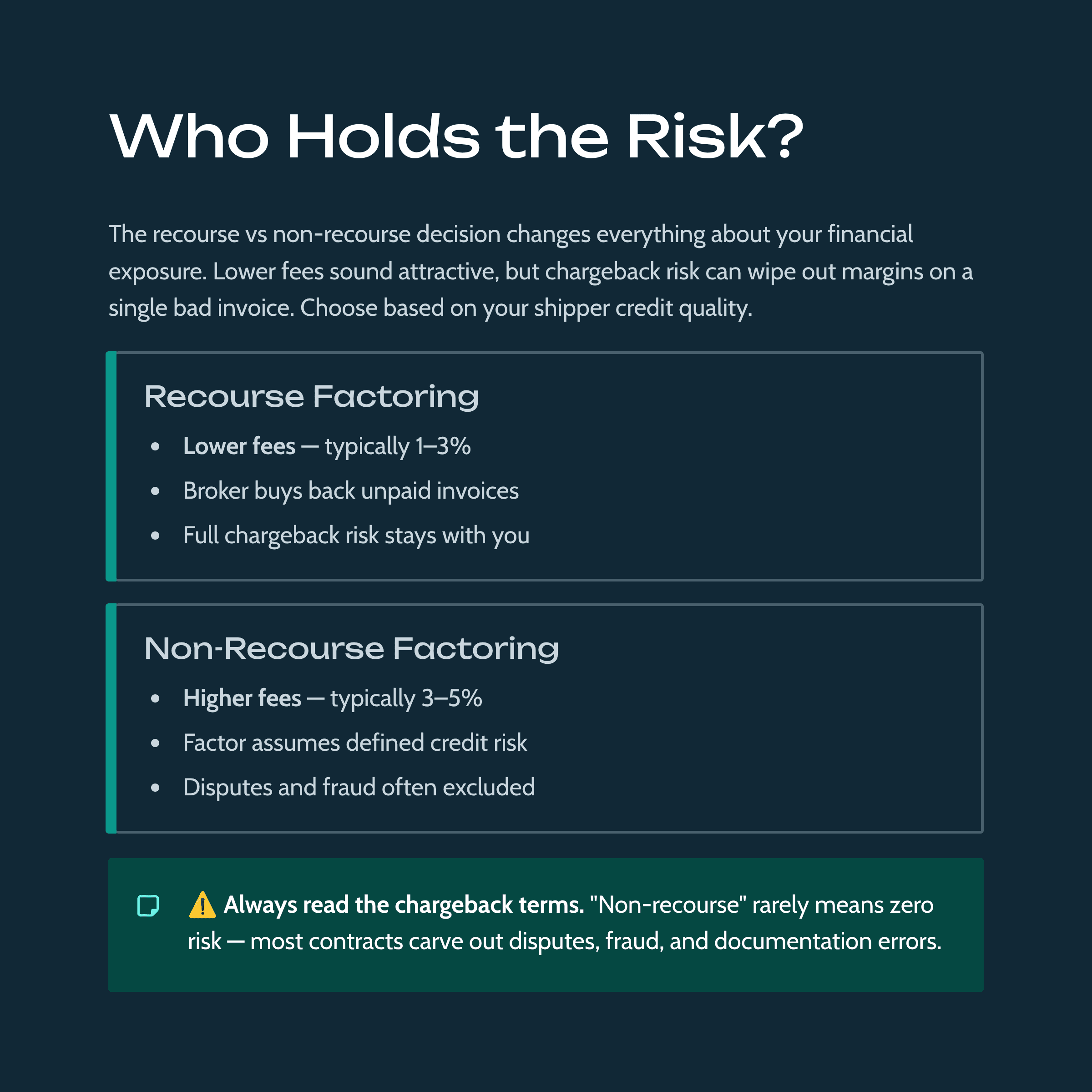

Recourse vs non-recourse

Recourse factoring: if the invoice doesn’t get paid, you’re ultimately on the hook (buyback/chargeback rules apply). Usually cheaper.

Non-recourse factoring: the factor takes on certain nonpayment risks, but read the definition carefully because “non-recourse” often applies to specific credit events (like insolvency) and does not cover disputes/claims. Usually costs more.

Contract gotchas to look for

These vary by provider, but you should explicitly ask about:

Monthly minimums

Termination fees and notice periods

Extra fees (wire/ACH fees, due diligence, invoice processing, etc.)

Whether the factor files a blanket lien vs A/R-only lien (ask your counsel to review)

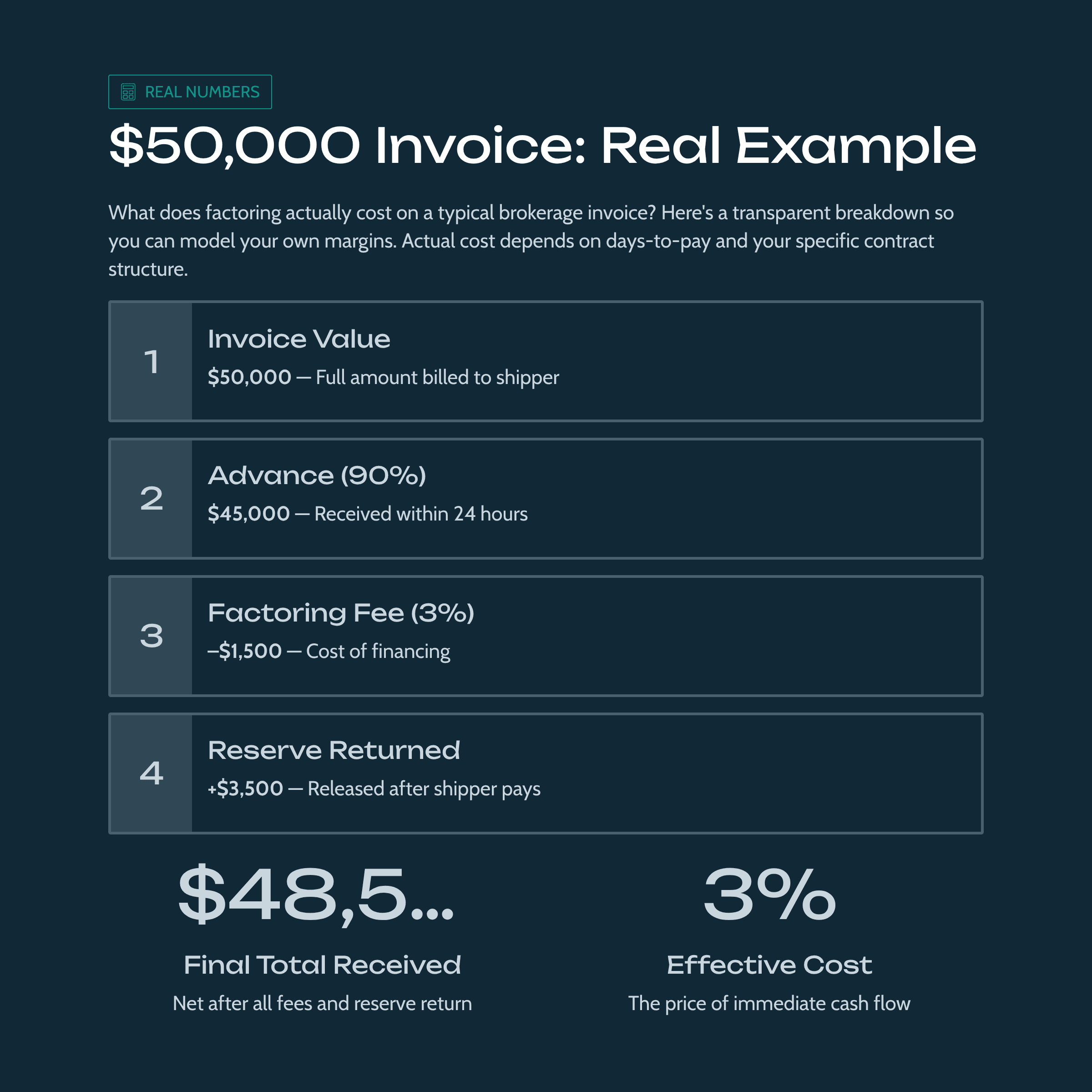

What does freight factoring cost? A real math example

Let’s make this concrete.

Scenario

Shipper invoice: $50,000

Advance rate: 90%

Reserve: 10%

Factoring fee: 3% per 30 days

Shipper pays in 30 days

Step 1: Advance

90% of $50,000 = $45,000 advanced to you.

Step 2: Fee

3% of $50,000 = $1,500 fee (for that 30-day period).

Step 3: Reserve release

Reserve held: 10% of $50,000 = $5,000

Reserve returned after payment (minus fee): $5,000 − $1,500 = $3,500

Total cash you received

$45,000 + $3,500 = $48,500

Total cost

$50,000 − $48,500 = $1,500 (3% in this simplified example)

This is the clean version. In real life, the “true cost” depends on how the provider calculates time, whether they charge weekly tiers, and what extra fees exist. Start your comparisons from the all-in cost, not the advertised rate.

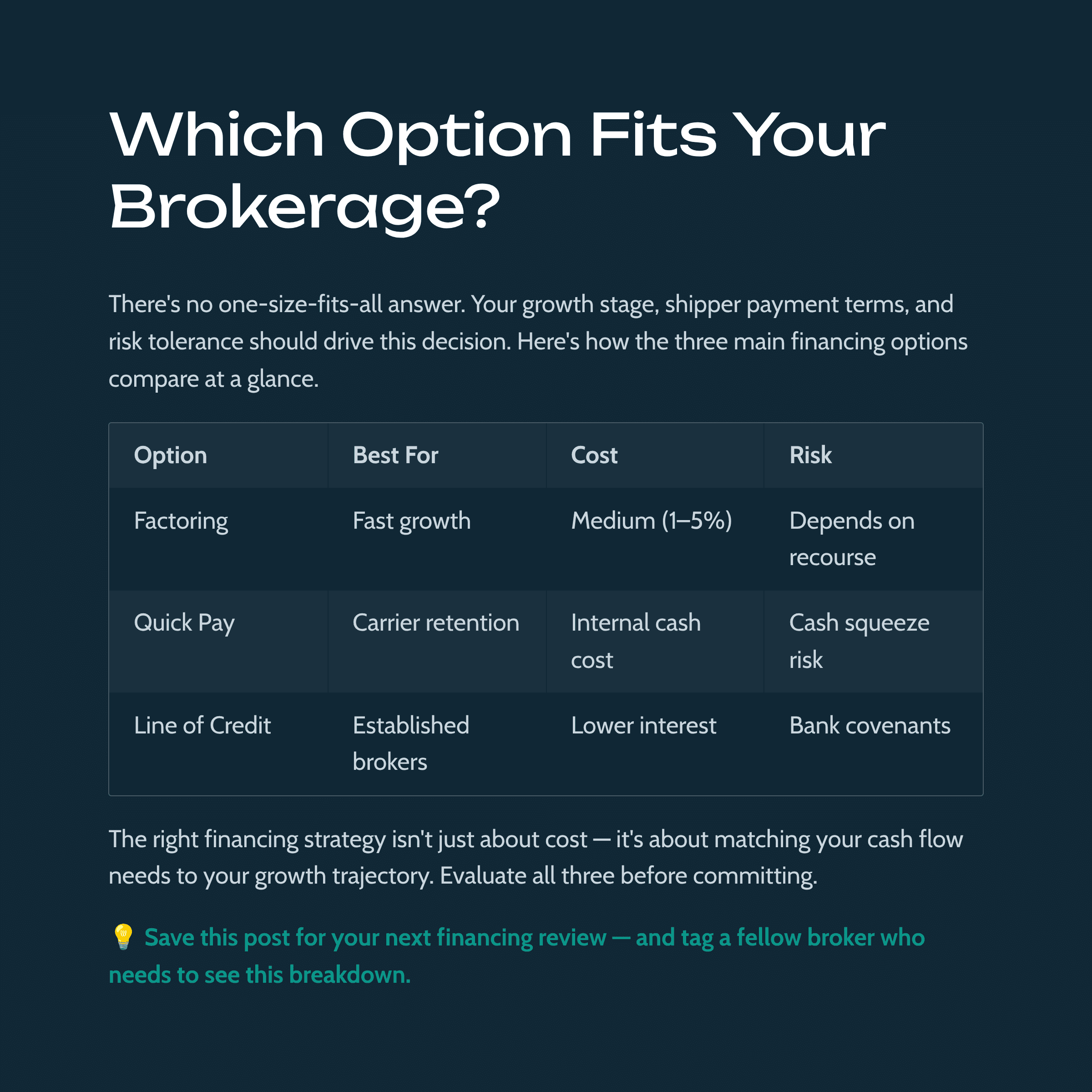

Freight factoring vs quick pay vs a bank line of credit

Brokers usually compare three options.

1) Freight factoring

Best for: fast growth, inconsistent cash flow, limited bank leverage, or when you want outsourced collections/back office support.

Tradeoff: you pay a discount fee and potentially give up some control of collections.

2) Quick pay programs (broker-funded)

Quick pay is typically a service you offer carriers to pay them sooner, usually for a fee. It helps with carrier loyalty, but it does not magically create cash. If your shipper pays late, quick pay can squeeze you.

3) Bank line of credit (A/R lending)

Best for: established brokerages with strong financials and clean books, where cheaper capital matters.

Tradeoff: covenants, reporting requirements, and approvals can be slower and less flexible than factoring.

A practical way to decide: if you’re primarily trying to remove the cash conversion gap and you want underwriting based on the shipper’s credit (not yours), factoring often fits.

How to choose a freight factoring company (broker checklist)

Don’t pick on rate alone. Pick on what can break your operation.

1) Shipper credit approval process

Ask:

Do you approve by shipper, by lane, or by invoice?

How fast are credit decisions?

What happens if the shipper is slow-pay but reliable?

Many factors evaluate the customer’s ability to pay as part of pricing and approval.

2) Funding speed and cutoff times

If you promise carriers quick pay, your factor’s funding speed becomes your reputation.

3) Recourse terms in plain English

Ask for:

Chargeback timing (day 60? day 90?)

What happens with short pays, claims, accessorial disputes?

4) Total fee transparency

You want an all-in list of:

discount fees

wire/ACH fees

monthly minimums

onboarding fees

termination fees

5) Back-office support

Some broker-focused programs include invoicing support, collections, and carrier payment services. That can be valuable if your team is lean.

6) Contract structure: spot vs ongoing

If your volume is uneven, ask if you can factor selectively (some programs allow invoice-by-invoice flexibility; others require all invoices).

Qualifying for broker freight factoring (what factors look at)

Factoring isn’t primarily about your credit score. It’s about your invoices and your customers.

Common qualification themes include:

You have invoices to creditworthy shippers (or brokers, depending on your model).

Your A/R is not already pledged in a way that blocks assignment (this is where a UCC filing review matters).

Expect to provide:

business formation docs

operating authority and broker details

sample invoices

customer list

bank info and proof of delivery documentation

Implementation: how to roll out factoring without chaos

If you want factoring to feel “invisible” to ops, you need a clean process.

1) Standardize your paperwork package

Have a checklist for every load:

rate confirmation

POD

accessorial documentation (if applicable)

invoice format consistency

The cleaner your package, the fewer delays and disputes.

2) Decide how shipper payments will work

In many factoring setups, payment direction changes (shipper pays the factor). Plan for:

updated remittance instructions on invoices

who communicates the change to the shipper

how you’ll handle “wrong pay” situations (shipper pays you by mistake)

3) Build a disputes SOP

Disputes are where factoring relationships get expensive. Have a written internal process for:

short pays

detention/accessorial disagreements

claim documentation

escalation timelines

2026 compliance notes brokers should not ignore

Factoring is finance, but you’re still a regulated broker. Two areas matter in 2026: records and financial responsibility.

Broker transaction records: 49 CFR 371.3

Brokers must keep transaction records and keep them for three years under the broker regulations.

Broker transparency rulemaking (still developing)

FMCSA has been working on changes that would strengthen how records are kept and provided, including concepts like electronic recordkeeping and a 48-hour response window upon request (as proposed in the NPRM materials). If this gets finalized later, it can change how quickly you must produce documentation and how you store it.

Bottom line: your factoring provider may touch invoicing and collections, but you still need your own compliance-ready records.

Financial responsibility: $75,000 bond or trust fund

Factoring does not replace your FMCSA financial security requirement.

FMCSA requires brokers to maintain $75,000 in financial security via a surety bond (BMC-84) or trust fund (BMC-85).

FMCSA also highlights that, effective January 16, 2026, brokers and providers have to comply with updated financial responsibility rules and enforcement mechanics (including suspension risk if security falls below the required amount and isn’t restored in time).

If you’re tying up cash in a BMC-85 trust fund, factoring can be one way to keep working capital available, but treat this as a planning conversation with your finance team, not a shortcut.

Taxes and bookkeeping in 2026 (quick, practical notes)

Factoring can change cash timing and who receives shipper payments, which affects reconciliation. Get your accounting workflows tight.

Two updates worth knowing:

1099 reporting threshold change (federal): The IRS has indicated the information reporting threshold for certain payments (including Forms 1099-NEC / 1099-MISC categories) increases from $600 to $2,000 for payments made after December 31, 2025, with inflation adjustments later.

Freight payment reporting exception: Treasury regulations include an exception for “payments of bills for… freight” in the 1099 reporting rules. This is real, but it’s also easy to misunderstand in practice, so don’t rely on blog posts (including this one) as your final answer. Have your CPA review how it applies to your exact payment structure.