Spot Rates in Trucking: What Freight Brokers Need to Know in 2026

Spot rates in 2026 are more volatile than ever. Learn what's driving pricing swings, how FMCSA's new bond rule affects brokers, and how to protect your margins

Omar Draz

Spot Rates in Trucking: What Freight Brokers Need to Know in 2026

If you've been brokering freight for any amount of time, you already know that spot rates don't move in straight lines. But 2026 is shaping up to be a year where the swings are sharper, the warning signs are harder to read, and the margin for error is thinner than it's been in a while.

This guide breaks down what's actually driving spot rate volatility right now, what the data says (not what the LinkedIn hot-takes say), and what freight brokers should be doing about it — lane by lane, load by load.

What Spot Rates Actually Are (and Why the Definition Matters More Than You Think)

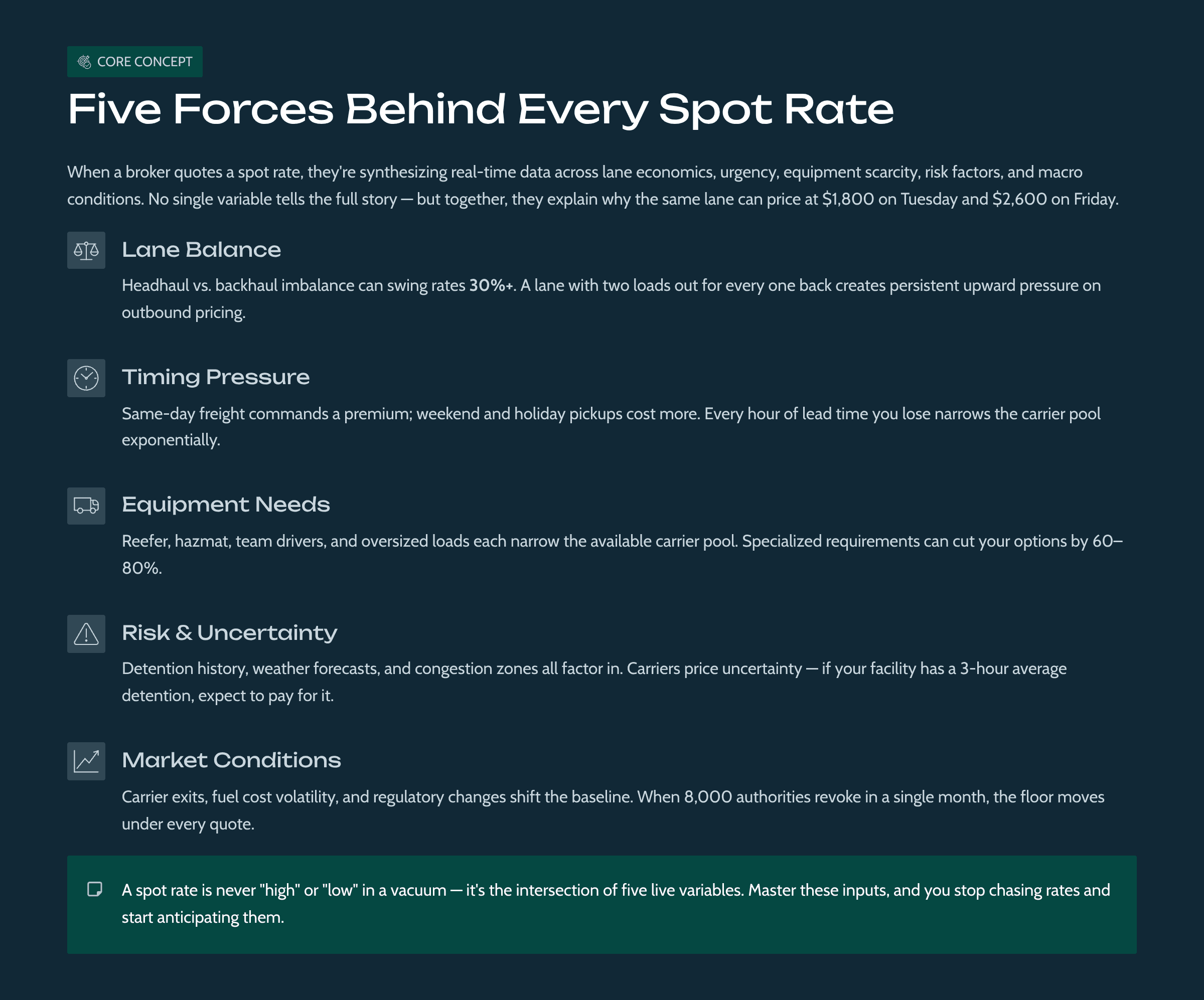

A spot rate is the price to move a specific load, right now, under today's conditions. That's it. It's not a published benchmark. It's not a national average. It's the number that a broker and a carrier agree on for one load, one lane, one pickup window — today.

That distinction matters because too many brokers treat spot rates like they're stable reference points. They're not. They're the output of a live negotiation that's sensitive to a surprisingly long list of variables.

What goes into a spot rate on any given day:

Lane-level supply and demand. Is this a headhaul or backhaul move? Is there a regional imbalance pushing trucks toward (or away from) the origin? Two lanes that look identical on a map can price 30% apart depending on repositioning economics.

Timing pressure. Same-day and next-day freight commands a premium. Weekend pickups, tight appointment windows, and after-hours dispatching all push rates up. The tighter the timeline, the fewer carriers can (or want to) say yes.

Equipment and service requirements. Reefer versus dry van. Team versus solo driver. Hazmat endorsement. Drop trailer versus live load. Each of these layers narrows the carrier pool and adjusts the price.

Risk factors. Weather forecasts, known congestion zones, detention history at specific facilities, and the likelihood of delays all feed into what a carrier is willing to accept. Experienced owner-operators price risk whether they articulate it that way or not.

The reason this matters for 2026 specifically is that several of these inputs are moving at the same time. Capacity is tighter in ways that aren't obvious from national averages. Fuel costs are shifting. Regulatory pressure is increasing. And weather keeps hitting the same system from multiple angles at once.

Before we get into what to do about it, let's look at what's actually happening in the market.

Why Spot Rates Are More Volatile in 2026

Carrier Capacity Is Fragile — and Can Tighten Overnight

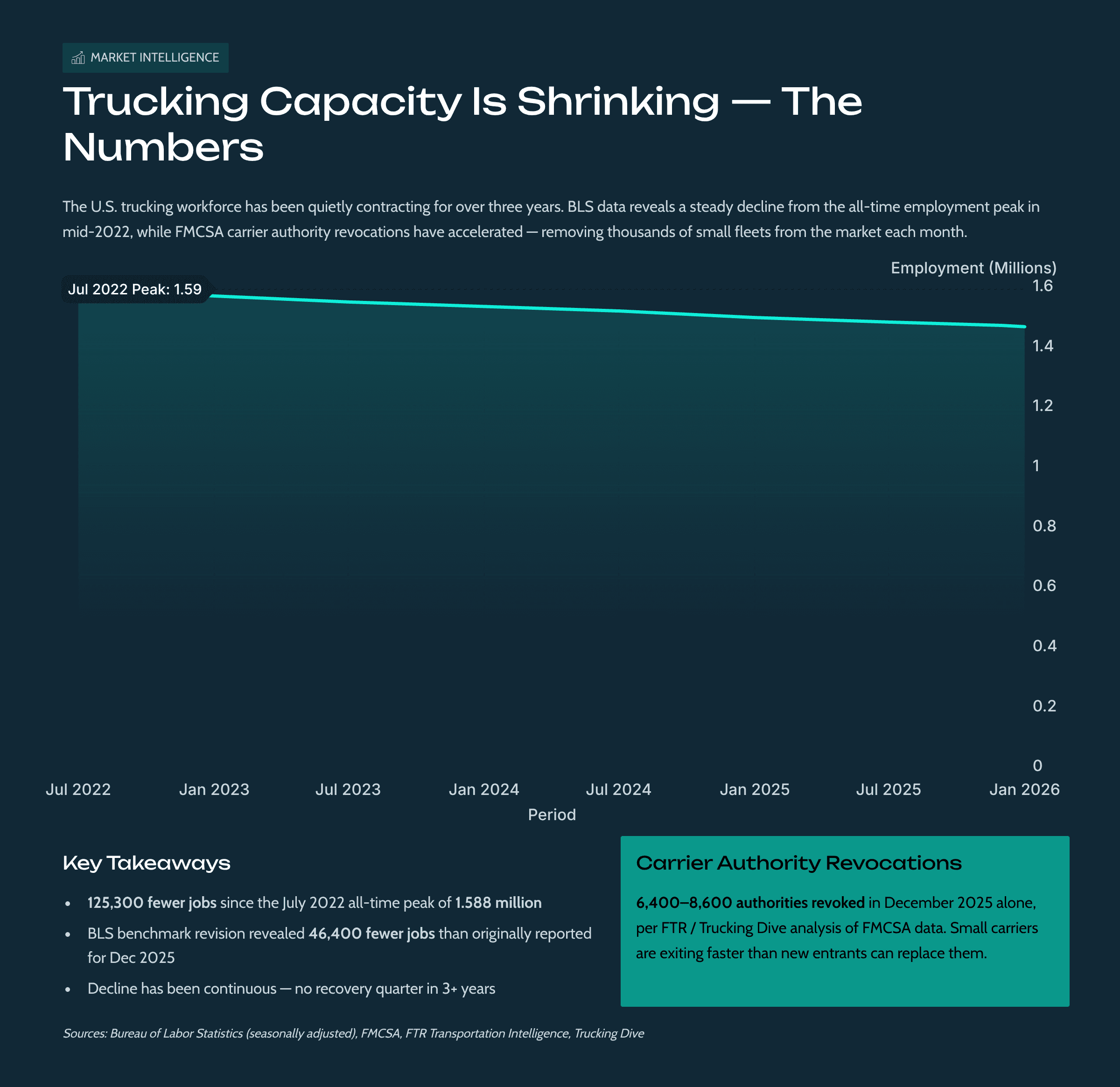

The freight recession that started in late 2022 pushed a lot of carriers out of business. But what's less discussed is that the exits didn't stop when rates stabilized — they kept going.

Trucking Dive's analysis of FMCSA operating authority data showed roughly 6,400 to 8,600 carrier revocations in December 2025 alone, depending on methodology. FTR's count came in around 6,400; Trucking Dive's own analysis put it closer to 8,600. Either way, that's a significant number of authorities being pulled out of the market in a single month.

On the employment side, the Bureau of Transportation Statistics reported that truck transportation employment fell to 1,462,600 in January 2026 — down 2.0% from January 2025 and down 0.3% from the previous month. That continued a trend that's been visible since mid-2023. For context, the all-time high for truck transportation jobs was 1,587,900 in July 2022. The industry has shed over 125,000 jobs from that peak.

FreightWaves noted that the Bureau of Labor Statistics' annual benchmark revision actually showed the decline was worse than originally reported. The revised December 2025 figure was 1,466,900 — some 46,400 jobs fewer than what had been reported just a month prior. In other words, the market was thinner than anyone thought, for most of 2025.

For brokers, this translates to a simple operational reality: capacity can tighten fast. A weather event, a regional surge in demand, or even a large shipper pulling forward freight can create spot rate spikes in lanes that looked balanced a week earlier. National averages will tell you the market is "soft." Your specific lane on a Tuesday afternoon might tell you something completely different.

Fuel: Lower on Average, Jumpier in Real Life

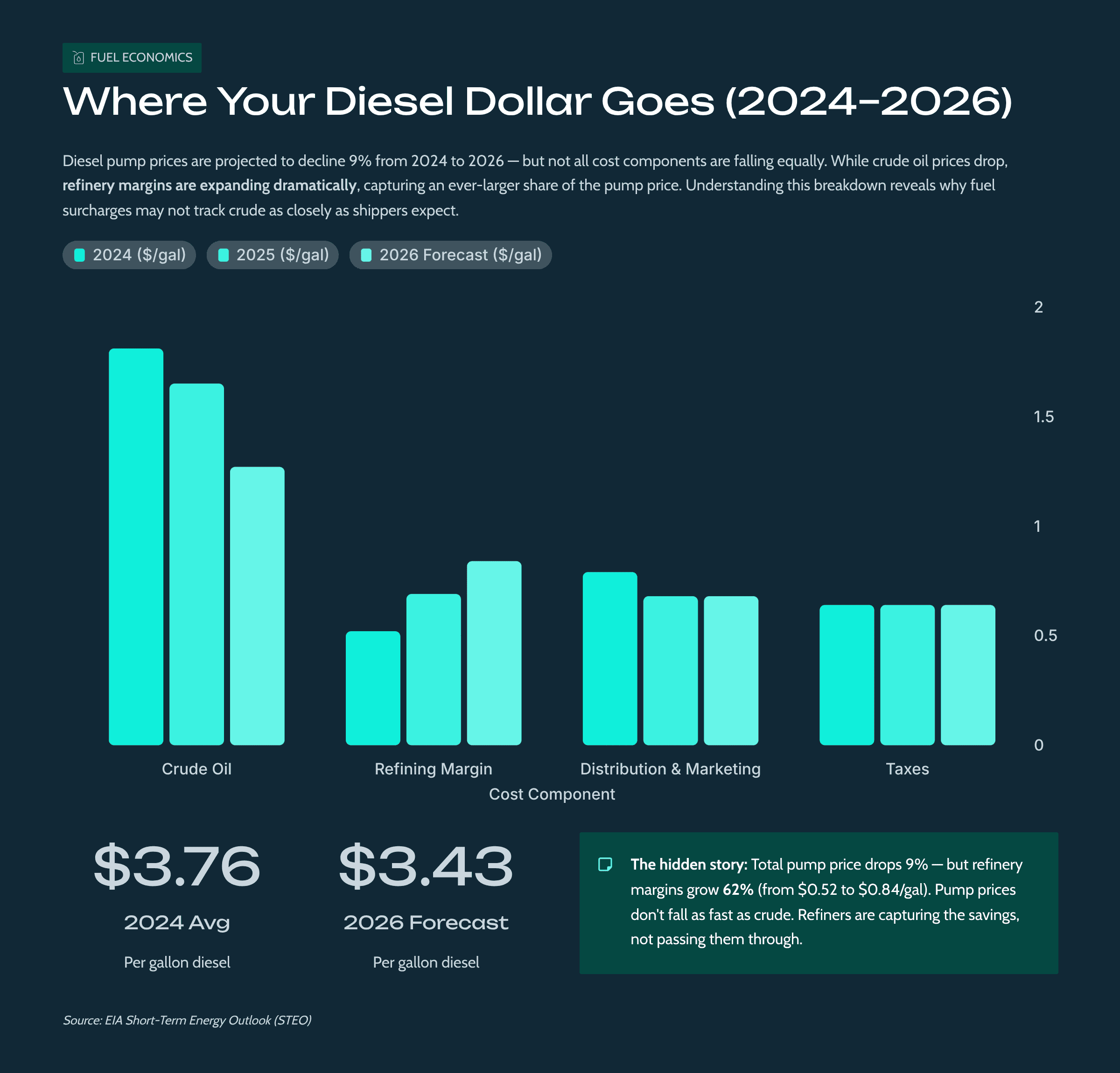

Diesel is still one of the biggest line items in a carrier's operating cost, which makes it one of the biggest inputs to spot pricing.

The EIA's Short-Term Energy Outlook projects the average U.S. retail diesel price at roughly $3.43 per gallon in 2026, down from $3.66 in 2025 and $3.76 in 2024. On the surface, that looks like relief.

But there are two things brokers need to pay attention to underneath that headline number.

First, the EIA also forecasts U.S. distillate fuel oil consumption (which includes diesel, renewable diesel, and biodiesel) to increase by around 2% in both 2026 and 2027, potentially reaching record highs by 2027. That forecast is driven by expectations of growing GDP, increased industrial activity, and more trucking miles. So demand for diesel is going up, even as the average price is projected to come down.

Second, the gap between crude oil costs and what you pay at the pump is widening. The EIA forecasts diesel crack spreads — essentially the refinery margin — to rise from about $0.52 per gallon in 2024 to $0.84 per gallon in 2026. That means even if crude prices drop significantly, refiners are capturing more of the benefit. Retail prices don't fall as fast as crude.

What this creates for spot rates is a "down on average, jumpy in real life" dynamic. The baseline cost of running a truck is slightly lower, which should ease some rate pressure. But because consumption is rising and refinery margins are widening, any disruption to the supply chain — a refinery outage, a pipeline issue, a cold snap that spikes heating fuel demand — can push diesel prices up fast in specific regions. And carriers will pass that through immediately on spot freight.

Freight Demand Is Uneven — and That's the Whole Point

One of the most frustrating things about 2026 for freight brokers is that national freight metrics will tell you one story, and your book of business will tell you another. That's because the economy isn't moving as one unit. Different sectors are pulling in completely different directions.

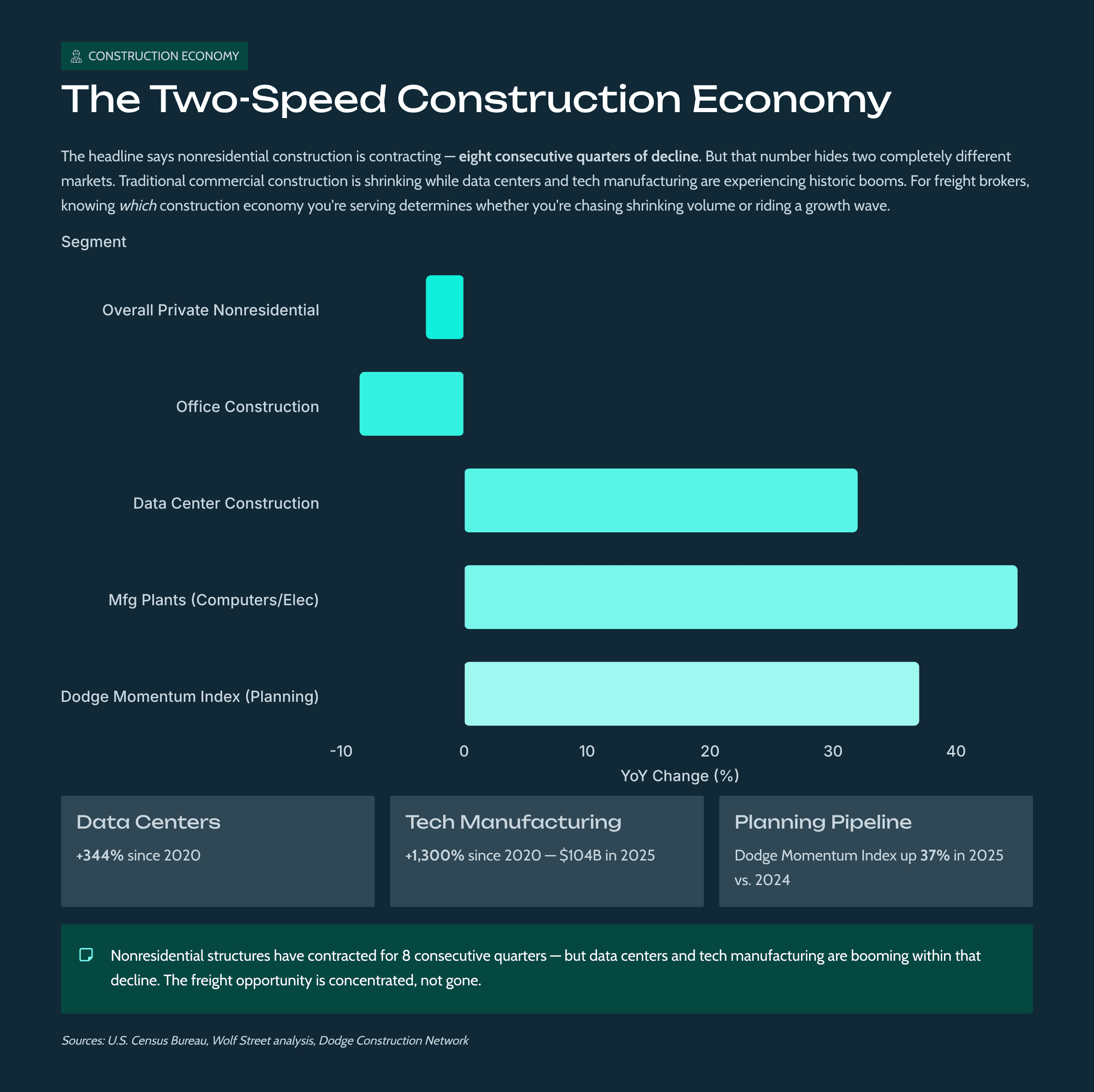

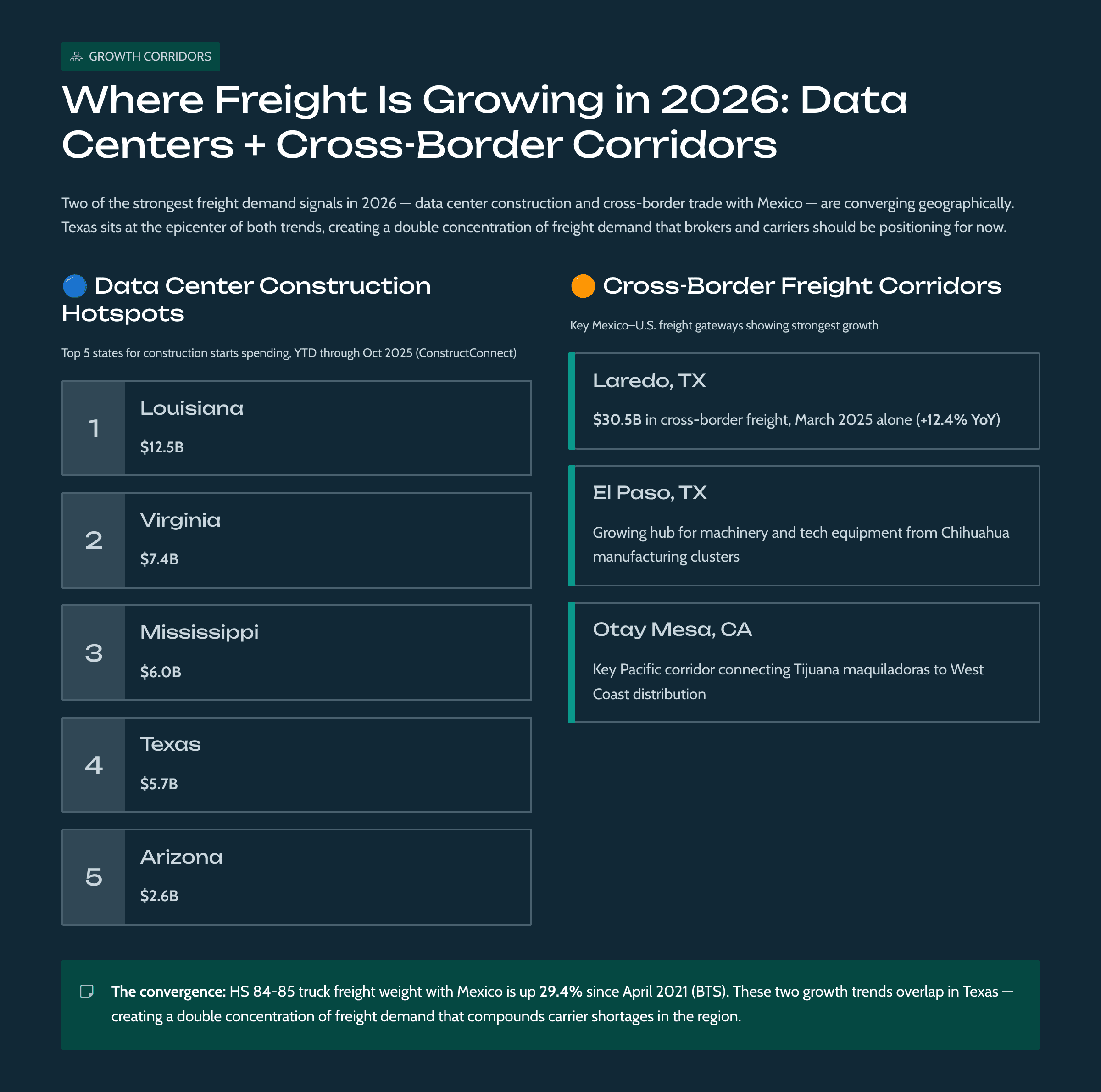

Construction is genuinely mixed. The Census Bureau's December 2025 construction spending data showed total spending up 0.3% month-over-month but down 0.4% year-over-year. Private nonresidential construction — offices, factories, commercial buildings — fell 0.7% in December and has now contracted for eight consecutive quarters. But within that decline, data center construction is exploding. Wolf Street's analysis of Census Bureau data showed data center construction spending hit $41 billion in 2025, up 32% from the prior year and up 344% from 2020. And spending on factories for computers, electronics, and electrical equipment — think semiconductor plants and AI infrastructure facilities — hit $104 billion in 2025, up 1,300% from 2020.

So "nonresidential construction is down" is technically true. But a freight broker who serves the data center or semiconductor supply chain is living in a completely different market than one hauling materials for traditional office or retail buildouts.

Cross-border truck freight with Mexico has structural tailwinds. The Bureau of Transportation Statistics published a data spotlight showing that the weight of truck freight in machinery and electrical categories (HS chapters 84-85) with Mexico surged 29.4% from April 2021 to May 2025 — from about 419,000 tons to nearly 543,000 tons. The comparable increase with Canada over the same period was 10.3%.

This is a nearshoring story that's actually showing up in freight data. Companies relocating manufacturing or assembly operations closer to the U.S. border are generating real, measurable increases in cross-border truck volumes. Laredo processed $30.5 billion in cross-border freight in March 2025 alone, up 12.4% year-over-year. El Paso is gaining traction as shippers move machinery and high-tech equipment produced in Chihuahua.

For brokers, this means specific corridors — Laredo, El Paso, Otay Mesa — are seeing sustained demand growth that's structural, not cyclical. If you're not building carrier relationships and operational expertise on those lanes, you're leaving money on the table.

AI-driven investment is creating concentrated freight demand. The Big Five tech companies alone — Amazon, Alphabet, Microsoft, Meta, and Oracle — announced plans for roughly $700 billion in combined capital expenditures for 2026, largely for AI-related infrastructure. That capital doesn't move itself. It turns into truckloads of servers, cooling equipment, electrical gear, construction materials, and specialized components flowing into specific geographies.

Dodge Construction Network's Momentum Index, which tracks projects entering the planning phase, finished 2025 up 37% compared to 2024. A significant portion of that growth came from data center projects in states like Louisiana, Virginia, Mississippi, Texas, and Arizona.

This is what "uneven demand" looks like in practice. Some lanes are quiet. Some corridors are running hot. And the hot ones tend to be concentrated enough that a broker who's positioned there can outperform the market, while a broker who's diversified across flat or declining sectors feels like rates are going nowhere.

Regulatory and Compliance Pressure Is Tightening — Especially for Brokers

This one deserves its own section because it's not just a market dynamic. It's an operational and financial survival issue.

The FMCSA Financial Responsibility Rule: What Actually Changed on January 16, 2026

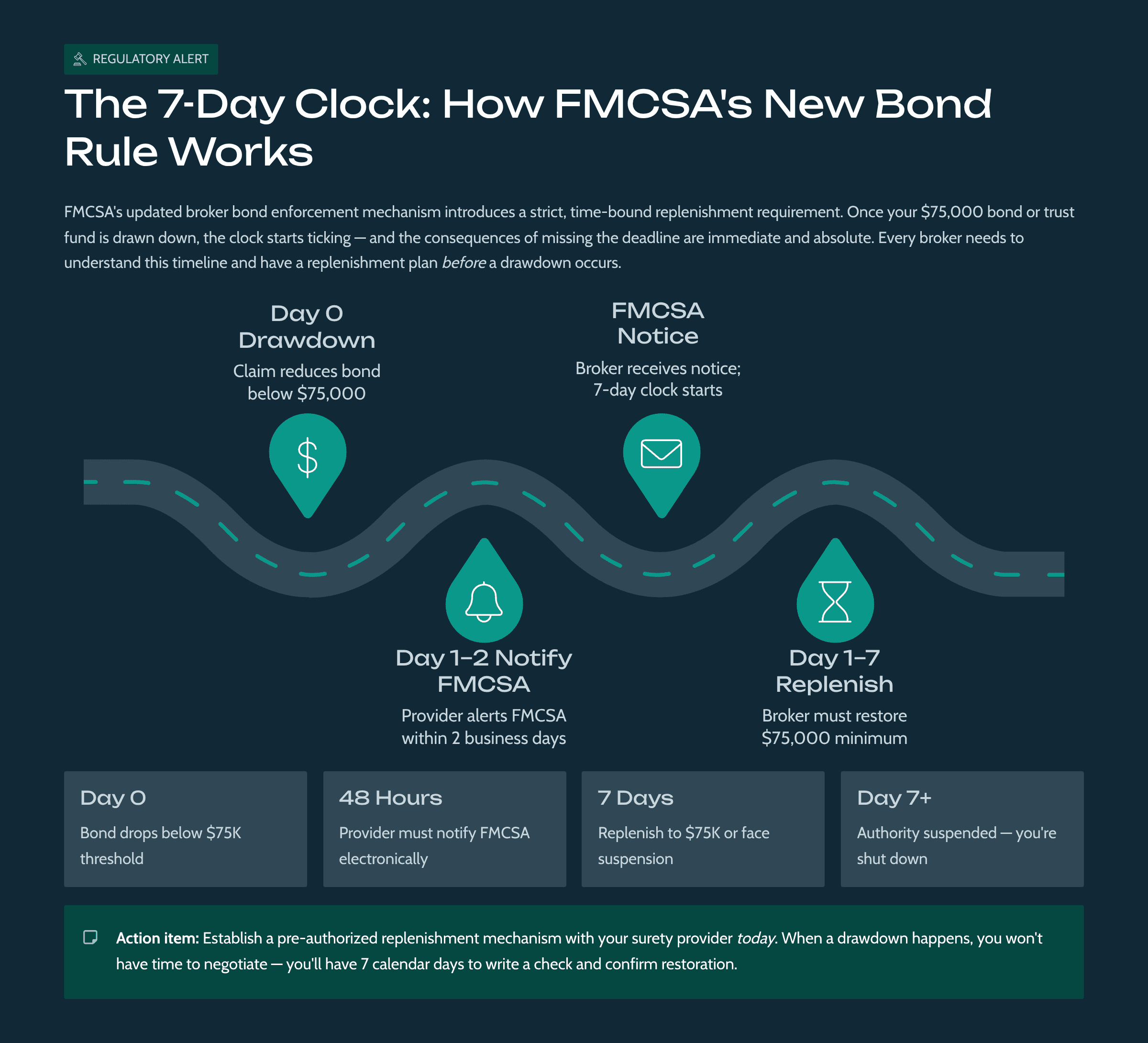

On January 16, 2026, the FMCSA's updated Broker and Freight Forwarder Financial Responsibility Rule went into full effect. This rule had been finalized back in November 2023 but was delayed a full year because FMCSA's new online registration system wasn't ready. Now it's live, and it fundamentally changes how broker financial security is enforced.

Here's what brokers need to understand:

The $75,000 bond is no longer a paper requirement. Under the old regime, if a broker's surety bond or trust fund dipped below the $75,000 minimum, there was often a long, informal grace period to sort things out. That's over. Under the new rule, if your available financial security falls below $75,000 and you don't replenish it within seven calendar days of FMCSA's notice, your operating authority gets suspended. Not warned. Suspended.

Your surety or trust provider must now notify FMCSA of drawdowns. Previously, lapses could go unreported for weeks or months. Now, surety providers (for BMC-84 bonds) and trust institutions (for BMC-85 trust funds) are required to electronically notify FMCSA within two business days when a broker's security drops below the threshold or when they determine a broker is experiencing financial failure.

The assets that count for BMC-85 trust funds are now restricted. The only acceptable assets are cash, irrevocable letters of credit from FDIC-insured institutions, and U.S. Treasury bonds. No more receivables, property deeds, cryptocurrency, or creative asset definitions. Additionally, loan and finance companies can no longer serve as BMC-85 trustees — only federally regulated financial institutions qualify.

Penalties for non-compliant providers are real. A surety company or financial institution that fails to comply faces a monetary penalty of $12,882 per violation and a mandatory three-year ban from providing broker financial security.

The timing is particularly challenging. Broker gross margins have been compressed for years. In a market where net revenues per load are already thin, even a single large claim — or a cluster of smaller ones — can wipe out the available portion of a $75,000 bond. Under the old rules, brokers had time to manage that quietly. Now, a depleted bond goes public within days.

What this means for your operations:

If your brokerage is well-capitalized and your claims management is tight, this rule is a competitive advantage. It cleans out underfunded competitors and raises the barrier to entry. But if you're operating with thin margins and no buffer plan, this is an existential risk.

Why Weather Moves Spot Rates (The Mechanics Most People Miss)

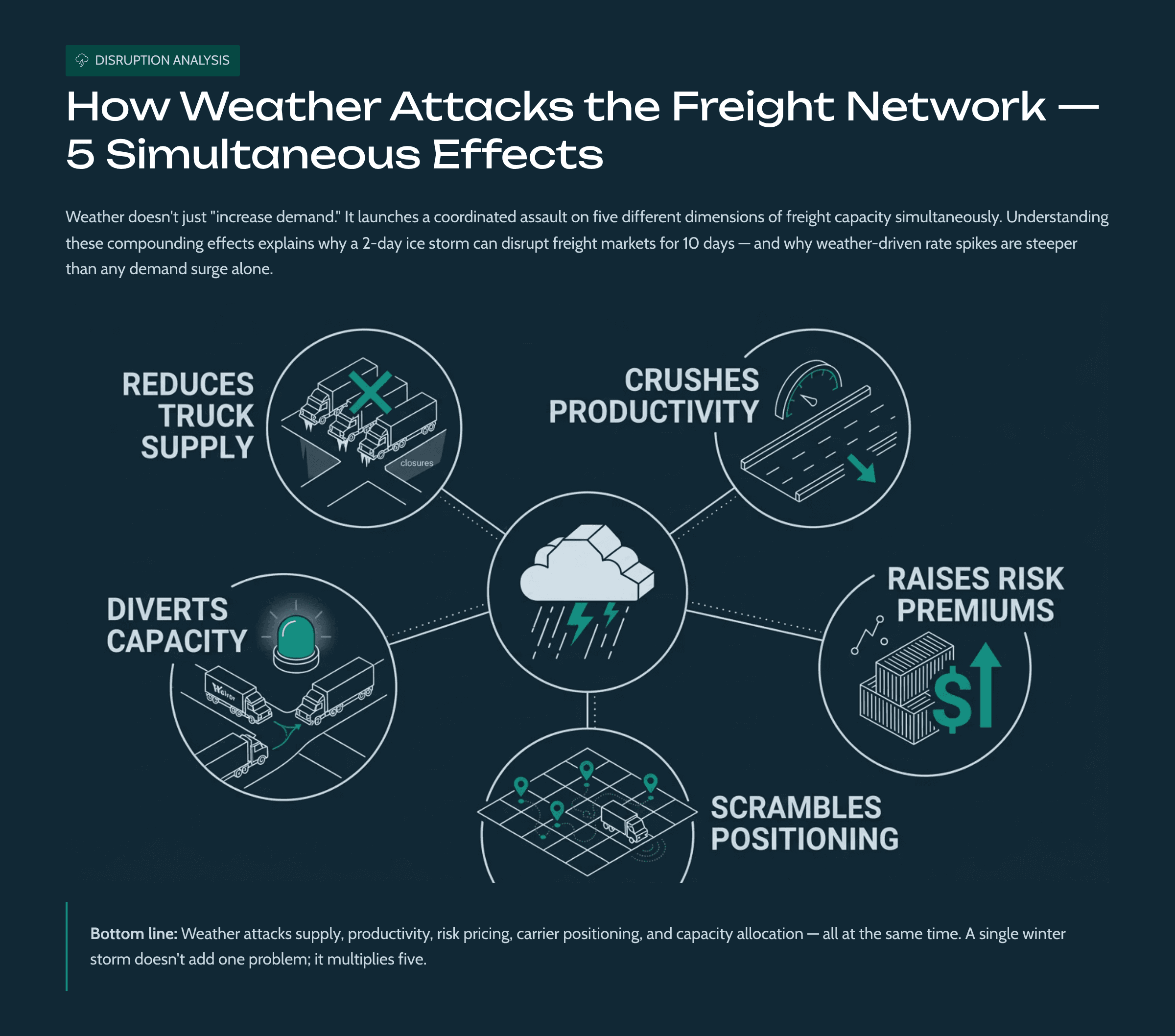

When people talk about weather and freight rates, the conversation usually stops at "demand goes up." That's true, but it's maybe 20% of the story. Weather attacks the trucking network from multiple directions simultaneously, and understanding the mechanics is what separates brokers who anticipate rate moves from brokers who scramble to cover them.

Weather Reduces Effective Truck Supply

When a winter storm hits a region, the number of trucks registered in the market doesn't change. But the number of trucks that can actually run changes dramatically. Snow, ice, extreme cold, high winds, and road closures all pull trucks off the road. Even trucks that are technically operational may be parked because their drivers don't want to risk it — and you can't blame them.

This is why a moderate storm in a major freight corridor can cause bigger rate spikes than a severe storm in a low-density area. The absolute number of trucks affected matters more than the severity of the weather.

Weather Crushes Productivity

Here's the part most people underestimate. Even when trucks keep running, they run slower. If transit time on a 500-mile lane stretches from one day to two days because of weather, every truck on that lane effectively handles half the loads it normally would. The market behaves as if it has fewer trucks, even though the actual count hasn't changed.

Multiply that across a region and you get cascading tightness. Trucks that were supposed to be available for a Tuesday load are still completing their Monday load. The system backs up.

Weather Increases Risk — and Carriers Price That In

A carrier accepting a load into a weather-affected area is pricing more than just the line-haul. They're pricing the risk of detention at a facility that's running behind because half their dock workers couldn't get to work. They're pricing the risk of a missed appointment and the deadhead that follows. They're pricing the increased odds of cargo claims if freight sits on a trailer longer than planned. And they're pricing the chance that after delivering, they'll be stuck in a region with no backhaul for days.

All of those risks get folded into the spot quote. That's why weather-driven rate spikes can exceed what you'd expect from a simple supply-demand analysis.

Weather Scrambles Positioning Networks

Trucks and trailers get stranded out of position during weather events. A driver who was supposed to deliver in Memphis and pick up a backhaul in Nashville might get stuck in Little Rock for two days. That means the Nashville load doesn't have a truck. And the truck that was supposed to follow that driver into Memphis from the other direction is also delayed. The cascading repositioning effects can ripple through a network for days after the weather clears.

Emergency Freight Can "Steal" Capacity from Routine Freight

This one became very real in early 2026. In January, FMCSA issued a Regional Emergency Declaration covering 40 states — Alabama through Wyoming — in response to severe winter storms and extreme cold. The declaration granted temporary hours-of-service relief for motor carriers providing direct assistance to emergency relief efforts. That HOS waiver was extended through February 20, 2026.

When an emergency declaration is active across 40 states, carriers who can move essential supplies — heating fuel, food, medical supplies — get regulatory relief that makes those loads more attractive. Routine commercial freight doesn't get that relief. So the available capacity for your standard dry van loads shrinks further, on top of everything else the weather is doing.

The bottom line: weather doesn't just increase demand for trucks. It reduces supply, slows the entire system, increases risk, disrupts positioning networks, and redirects capacity toward emergency freight — all at the same time. That's why weather-driven spot rate spikes can be so sharp and so fast.

What Freight Brokers Should Actually Do in 2026

Understanding the market dynamics is one thing. Translating them into operational decisions is another. Here's what separates brokers who thrive in volatile conditions from brokers who just survive them.

1. Treat Every Spot Quote as a Risk-Managed Offer

In stable markets, you can quote a rate in the morning and feel reasonably confident it holds until the afternoon. In 2026's conditions, that assumption will cost you money.

Use tight quote validity windows. When weather is active, regional capacity is shifting, or you're quoting into a lane that's been volatile, your quote validity should be hours, not days. Make this explicit to shippers: "This rate is valid until 3 PM today."

Quote with explicit assumptions. Don't just send a rate. Send a rate with conditions: "Assumes 2-hour pickup window, live unload, no appointment changes, standard 48-foot dry van." When any of those assumptions change, the rate changes. Putting this in writing protects you and sets expectations.

Build re-rate triggers into your SOPs. Define the conditions under which your team must re-rate a load before dispatching: a weather advisory issued after the quote, a multi-state emergency declaration, a facility delay reported by the last three carriers, an appointment time change. If you wait for someone to "feel" like the rate is wrong, you're already losing money.

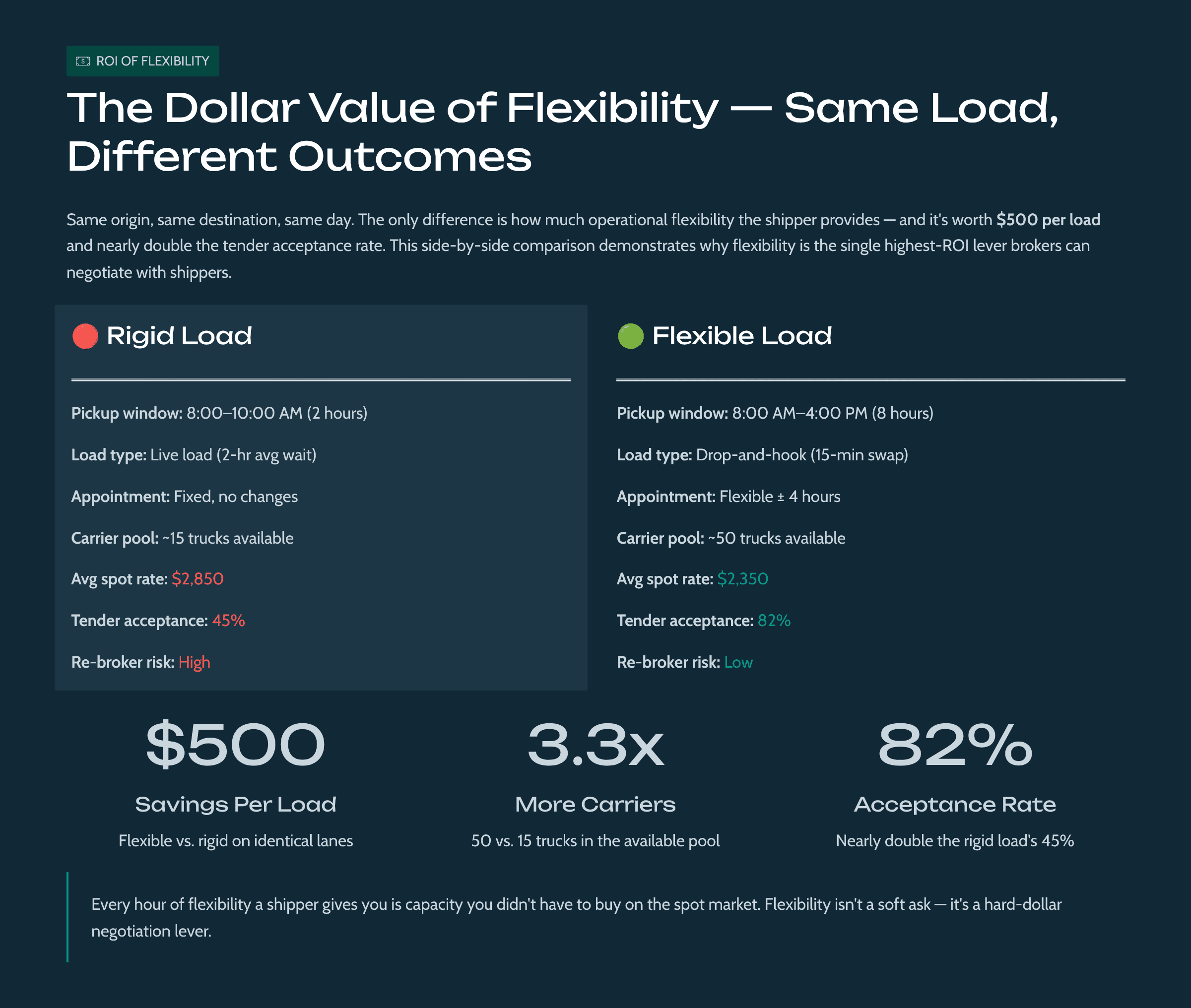

2. Sell Flexibility to Shippers Before You Sell Price

Here's something that sounds obvious but most brokerages don't operationalize: every hour of flexibility a shipper gives you on pickup or delivery is effectively extra capacity you didn't have to pay for.

When a shipper says "I need this picked up between 8 and 10 AM," your carrier pool is X. When they say "I need this picked up today," your carrier pool is 3X. That expanded pool means more competitive rates, higher acceptance rates, and fewer re-brokers.

Practical moves:

Push for wider pickup windows — even an extra two hours makes a meaningful difference in carrier acceptance

Advocate for drop-and-hook wherever possible — it turns a two-hour live load into a 15-minute swap, which carriers love

Work with shippers on detention discipline — if their facilities are chronically slow, help them fix it or at least acknowledge the cost

Rethink appointment strategies — "earliest possible" isn't always best. Sometimes a slightly later appointment that avoids the morning rush means higher on-time performance and lower carrier frustration

3. Build a Real Weather Playbook

Not a vague awareness that weather affects freight. An actual documented playbook that your ops team can execute without improvising.

Your playbook should answer:

At what point do we stop accepting commitments into affected lanes? (Define specific triggers: NWS winter storm warnings, state emergency declarations, FMCSA regional declarations.)

When do we pre-book capacity ahead of the storm zone? (If a major storm is forecast for Thursday, are you locking in trucks Tuesday for Friday delivery?)

What are the lane detours and alternates? (If I-70 through the Rockies closes, what's my fallback? How much does the alternate route add to transit and cost?)

What accessorials are mandatory during events? (Tarp charges, detention pre-approval, layover authorization — who approves these, and up to what amount?)

What are the customer communication templates? (Proactive delay notices, decision-point emails with options, escalation paths.)

The FMCSA's 40-state winter emergency declaration in January 2026 is proof that weather events can be broad enough to affect half the country at once. That's not a "deal with it when it happens" scenario. That's a "we need a plan and we need it before the season starts" scenario.

4. Make Carrier Relationships a System, Not a Vibe

In a capacity-constrained environment, carriers have choices. They will prioritize brokers who make their lives easier. This isn't about being "nice" — it's about being operationally excellent in ways that reduce carrier friction.

What carriers actually care about:

Clean tenders with accurate details. Nothing burns trust faster than showing up to a pickup and finding the load is different from what was tendered. Weight, dimensions, commodity, appointment time, facility instructions — get it right the first time.

No appointment surprises. If the appointment changes, tell the carrier immediately. Don't wait until they're two hours away.

Fast payment and clean resolution. Carriers remember who pays in 15 days and who pays in 45. They also remember who fights them on legitimate detention, TONU, and layover claims.

Honest communication. If a load is going to be difficult — long wait times, tight dock, unreliable facility — say so upfront. Carriers respect honesty more than they resent difficulty.

Build this into your operations:

Reduce "blast" tenders. Target specific carriers based on lane performance history.

Maintain a short list of preferred carriers by lane with actual performance notes — not just "they've hauled for us before," but "averages 98% on-time pickup in this lane, prefers appointments after 10 AM."

Proactively ask your best carriers what makes a load a "no-go" for them, then design around those friction points.

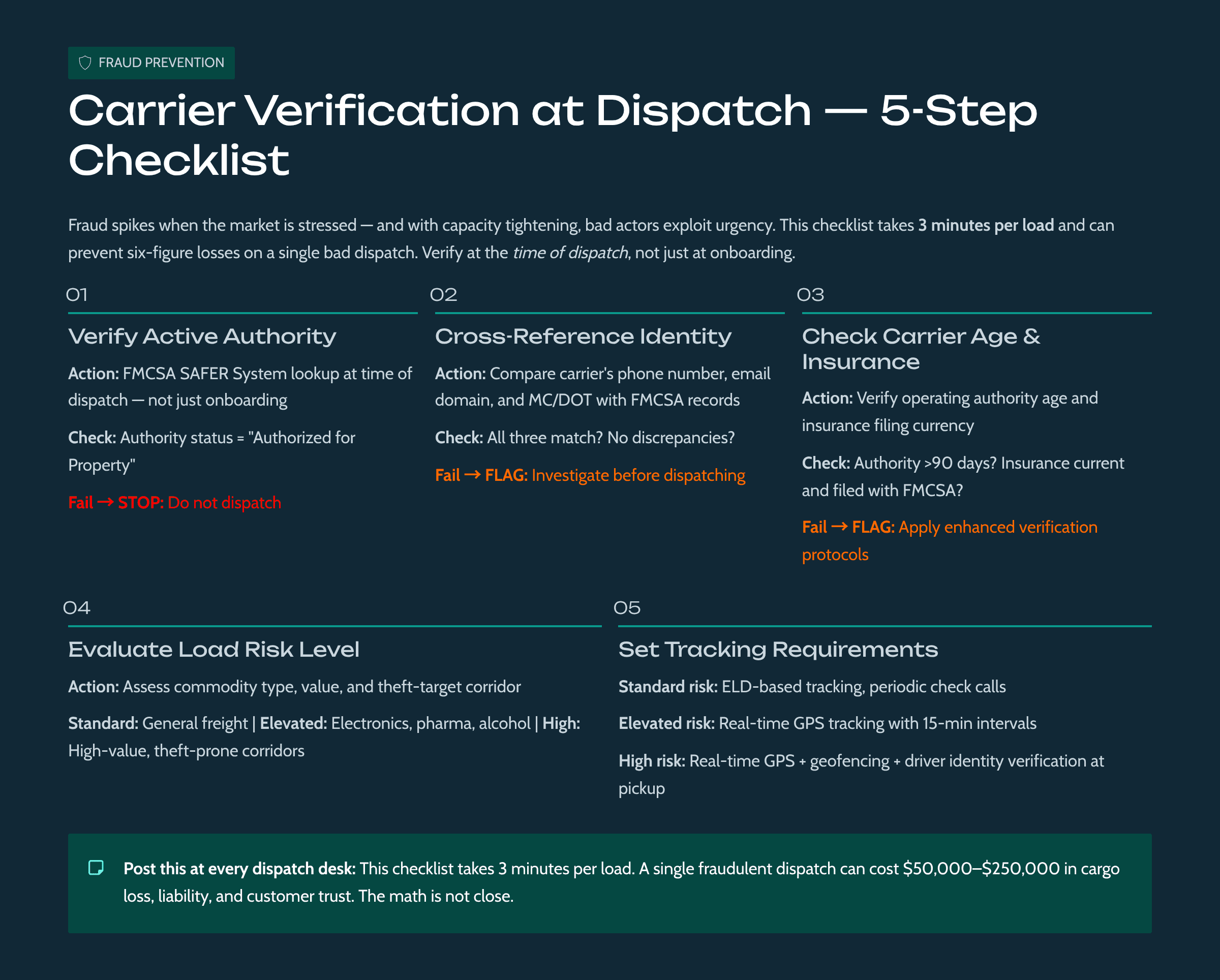

5. Tighten Fraud and Authority Controls

When the market is stressed, freight fraud increases. Double brokering, identity fraud, and cargo theft all tend to spike when carriers are under financial pressure and when desperate brokers are scrambling for capacity.

Minimum standards for 2026:

Verify active operating authority on every load. Don't just check at onboarding — check at dispatch. FMCSA's revocation dataset is publicly available and updated frequently through the DOT's open-data catalog.

Match carrier identity across multiple signals. The phone number they're answering, the email domain they're using, and the FMCSA records should all tell a consistent story. Discrepancies are red flags.

Require tracking compliance that matches the freight risk. High-value or theft-target commodities need real-time GPS tracking with geofencing, not a "call check" every four hours.

Watch for the warning signs of double brokering. If a carrier you've never worked with accepts a load instantly at a rate well below market, ask questions before you dispatch.

6. Treat FMCSA Financial Responsibility as a Zero-Failure Item

This is not compliance paperwork. This is business continuity.

What to do right now:

Set an owner-level KPI on never letting your financial security dip below $75,000. This should be monitored weekly at minimum.

Maintain a buffer plan. Know exactly where you'd access liquidity — a line of credit, reserve funds, personal guarantee — to replenish your bond within days if a claim draws it down. Have the authorization pre-arranged so you don't waste two of your seven days getting internal approvals.

Respond to claims correspondence immediately. Under the new rule, if a surety or trust provider sends you a claim notice and you don't respond, they can determine the claim is valid and pay it — drawing down your bond. A slow response can trigger a cascade that ends with your authority suspended.

Know your surety provider's compliance status. The new rule restricts who can serve as BMC-85 trustees. Up to 90% of previous trust providers may not qualify under the new asset requirements. Verify that your provider has filed properly and meets the new standards. If they don't, your bond isn't valid even if you think it is.

7. Shift Your Customer Mix Toward Structured Spot

Pure transactional spot is the highest-margin-volatility segment of the freight market. One week you're making 20% gross margin, the next week you're losing 5%. In 2026's conditions, that roller coaster is even more extreme.

A better approach is to build toward structured spot programs that still let you participate in spot pricing but reduce the chaos:

Mini-bids with short refresh cycles. Instead of one annual RFP, run quarterly or even monthly bids on your core lanes. Shippers get current pricing; you get more predictable volume.

Surge-cap terms. Pre-define with your shippers what happens when rates spike beyond a certain threshold. "If the spot rate on this lane exceeds contract by more than 25%, we'll split the overage 50/50." It's not a perfect solution, but it keeps both parties at the table instead of re-negotiating every load.

Volume commitments with flexibility clauses. Commit to a shipper's volume in exchange for flexibility on timing, mode, or routing. You're essentially trading their commitment for your operational latitude.

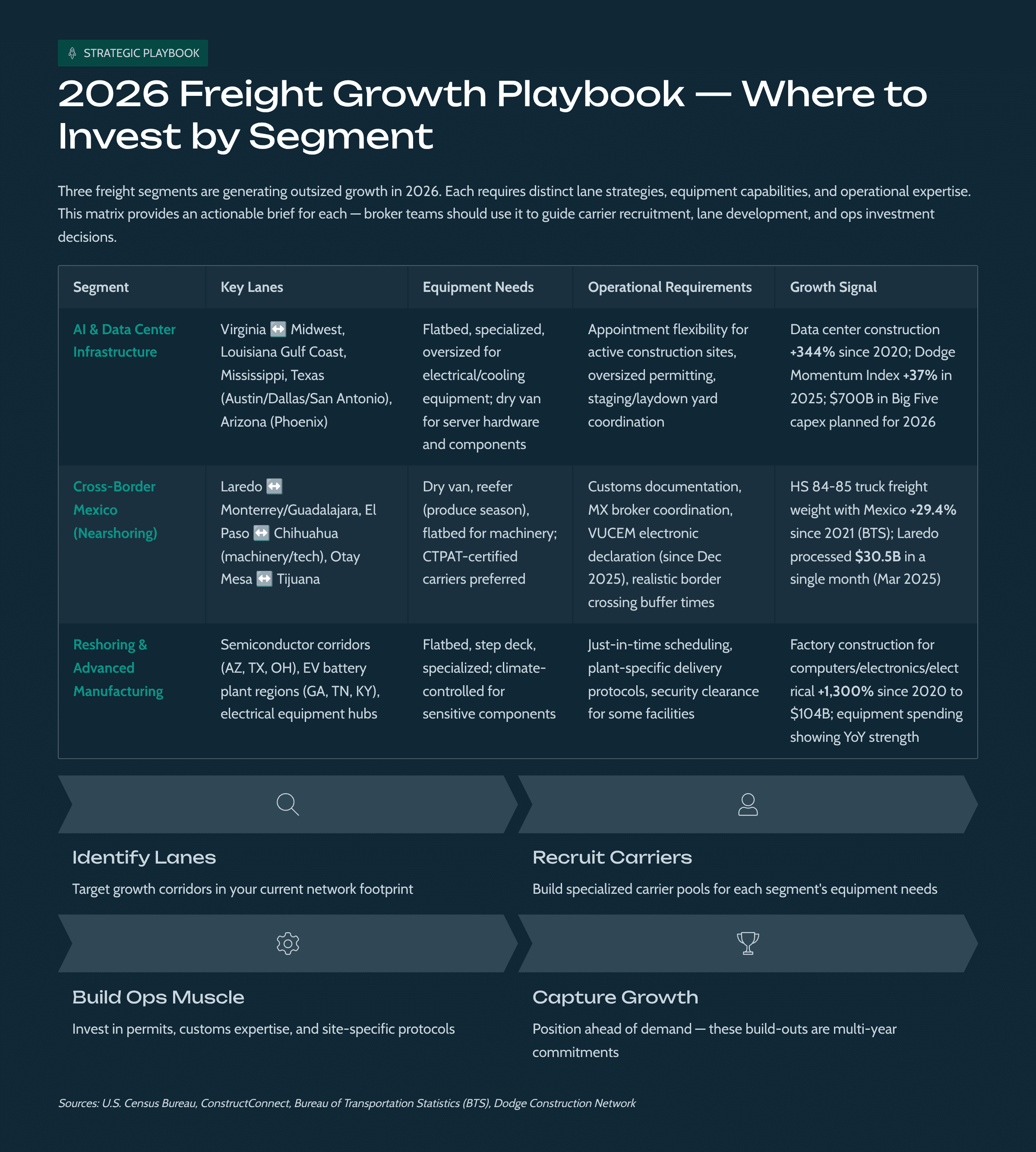

8. Align to Where Freight Is Actually Growing

Don't build your 2026 strategy around 2024's freight map. The lanes that are growing in 2026 look different from where freight was concentrated two or three years ago.

Where the growth is:

AI infrastructure corridors. Data center construction is driving freight into specific states — Louisiana, Virginia, Mississippi, Texas, Arizona are the current hotspots. That's not just construction materials; it's specialized electrical equipment, cooling systems, power generation components, and server hardware.

Cross-border Mexico lanes. The machinery and electrical freight growth with Mexico is real (29.4% weight increase over four years per BTS data) and structural. Laredo, El Paso, and Otay Mesa are the primary corridors. Brokers who can handle the documentation requirements, appointment realities, and buffer time needed for cross-border moves have a growing addressable market.

Manufacturing tied to reshoring and nearshoring. Equipment spending in sectors tied to domestic production — particularly electronics, semiconductors, and electrical equipment — is creating lane-specific demand that's independent of the broader economic cycle.

What this means operationally:

Build carrier capacity on growth corridors, not just on the lanes you've always run.

Invest in cross-border operational competence: documentation, customs, appointment flexibility, and realistic transit expectations.

Price these lanes based on their specific economics, not on national average benchmarks. A national average is useless for a lane from Laredo to Dallas that's running 15% above the rest of Texas.

Putting It All Together

Spot rates in 2026 aren't just "higher" or "lower." They're more reactive. The system has less slack — fewer carriers, thinner margins, tighter regulatory timelines, and concentrated demand growth — which means any disruption moves prices faster and farther than it would in a looser market.

For freight brokers, the playbook comes down to a few core principles:

Volatility is the default condition. Stop treating rate spikes as surprises and start treating them as the expected pattern. Build your quoting, your SOPs, and your customer agreements around the assumption that rates will move — and that you need to be positioned to respond quickly without giving away margin.

Flexibility has a dollar value — price it. Every hour of pickup flexibility, every drop-and-hook opportunity, every detention-free facility is capacity you didn't have to buy on the spot market. Make this case to your shippers in dollars, not in abstract terms.

Carriers are scarce inventory, not interchangeable commodity. In a market where 125,000 jobs have disappeared from the peak and thousands of authorities are being revoked each month, the carriers you work with are strategic assets. Treat them accordingly — clean tenders, fast pay, honest communication, and no games.

Compliance is existential. With seven days between a bond drawdown and authority suspension, there is no room for "we'll get to it." Financial responsibility, carrier verification, and fraud prevention aren't back-office functions anymore. They're front-line business continuity operations.

Go where the freight is growing. National averages are noise. The signal is in the corridors: data center buildouts, cross-border Mexico, AI-driven manufacturing. Position your brokerage on those lanes and build the operational muscle to serve them.

The brokers who win in 2026 won't be the ones who predict the market correctly every day. They'll be the ones who built the systems, relationships, and operational discipline to handle whatever the market throws at them — and come out on the other side with their authority intact, their carriers loyal, and their margins protected.

Sources referenced in this article include the Bureau of Transportation Statistics, the U.S. Bureau of Labor Statistics (Current Employment Statistics), the U.S. Energy Information Administration's Short-Term Energy Outlook, FMCSA emergency declarations and financial responsibility rule documentation, U.S. Census Bureau construction spending data, Trucking Dive's analysis of FMCSA operating authority data, FreightWaves, and Dodge Construction Network.